They will not get the house as component of their inheritance. Reverse home mortgages are also high-risk in regards to scams, as well as many borrowers succumb predatory methods that can cost them significant amounts of cash or the home itself. If you select a government backed choice, you will certainly additionally be required to pay mortgage insurance policy premiums. These expenses can be taken out of the financing amount, so you do not have to pay them expense, yet they will minimize just how much money you get after closing.

A house evaluation is constantly required as component of the reverse home mortgage process to get an unbiased point of view of your house's value from a certified property evaluator. Seniors need to have the time to effectively evaluate their decision to obtain a reverse home mortgage. When elders purchase an annuity they generally have 10 days to evaluate the decision as well as terminate without a fine. In The golden state, this "complimentary look" duration lasts for thirty days.

To get as well as keep your FHA-insured HECM, you have to pay a 1.25 percent premium every year on your finance balance. For a reverse mortgage, they can run as long as $15,000. You've heard about it, however do you know what a reverse home loan is? Right here are reasons why you should not get a reverse home loan.

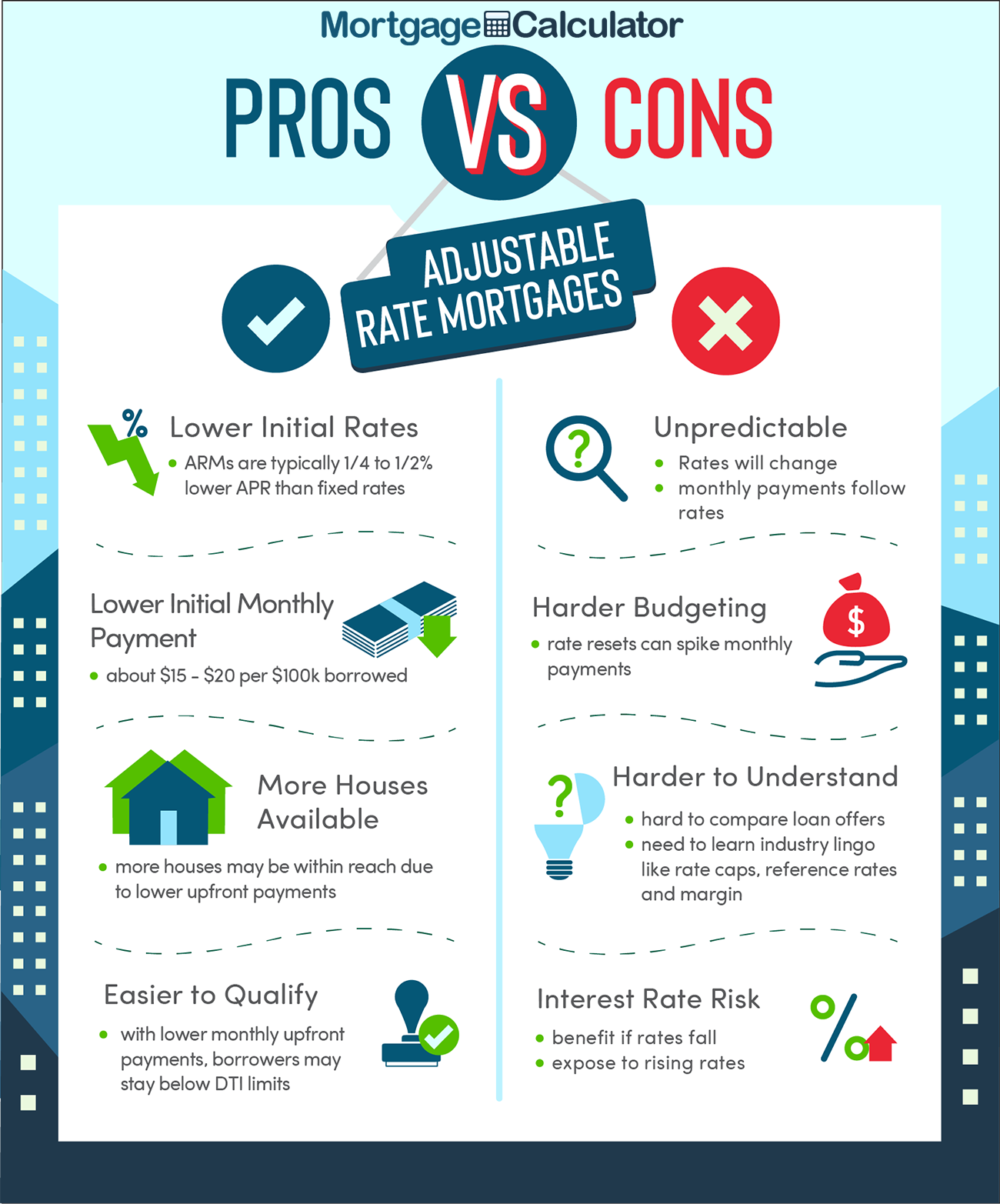

In the ideal situations, a reverse mortgage can be a source of badly-needed money in an individual's retirement years. On the other hand, http://tituseazy231.theglensecret.com/what-is-a-mortgage-fundamentals-for-initially there are some negative elements to turn around mortgages. Remember that you have various other alternatives to gain access to money, also. Contrast a house equity funding versus a reverse Learn here mortgage to see which one is a better fit for your needs. Record-low rates of interest-- While rates of interest are beginning to climb and will likely continue that path in 2022, it's still an economical time to obtain money.

- You may intend to talk to an economic expert and also your household prior to obtaining a reverse mortgage.

- We are lately retired yet still with a home with a $300k home mortgage left.

- Prior to you get a reverse home mortgage, make sure you review the advantages and disadvantages.

- She is driven to offer clients, participants, and also students with crucial knowledge, skills, and approaches to navigate the typically potholed monetary roadway ahead.

- As opposed to passion intensifying on a lower number each month, like a normal mortgage, reverse home mortgages substance on a higher number because of the added premiums.

If you maintain the loan-to-value ratio fairly low as well as you have a good credit history score, you have an outstanding possibility of getting accepted. If you learn your outstanding costs are hindering loan authorization, you can choose to "settle financial obligation to qualify,"-- which means applying some or every one of your lending continues to outstanding debts at closing. Understanding the advantages and disadvantages of reverse home loans is simply the start. As a potential HECM applicant, you should complete reverse home loan counseling with a HUD-approved therapist prior to you can proceed with an application.

You'll also get billed approximately $30 to $35 monthly as a service charge. If you are anticipated to live one more one decade you'll be charged an additional $3,600 to $4,200. That figure will certainly be subtracted from the amount you receive.

People who need even more money in retired life nowadays may be taking into consideration a reverse mortgage. If your home falls in value, the reverse mortgage lending institution takes the loss. The options for moneying one's retirement are varied and wide-ranging. Using home equity as retirement income can be an intriguing choice for retiring Canadian infant boomers who have taken advantage of solid property markets over the past twenty years. By Family Caretaker Alliance Kathy, age 59, dislikes tom matthews wfg to see her mother Betty battle with financial restrictions.

Reverse Home Mortgages: The Good And The Poor

Lenders might take a look at other factors that enter play when you obtain a traditional funding, like your credit score and also debt-to-income ratio. But the DTI is not usually thought about in the certification. Any individual that blindly thinks what they hear advertised shouldn't be anywhere near the conversations on reverse home mortgages.

The Suitable Consumer

It's additionally worth considering what may occur to home rates. " If residential property prices decrease, equity will certainly be subsumed faster," states Pedersen-McKinnon. " Australian retirees possess over $1 trillion in house equity, and we require to locate methods to permit them to access that to money their retired life," states Home Resources president Josh Funder. The amount you can obtain is a feature of your age and also the worth of your home. The finance to value proportion begins at 15% at age 60 before enhancing in about 1% increments each year.

When Do You Repay A Reverse Mortgage?

The majority of counseling sessions happen over the phone and it can be tough for elders and also those who are listening to damaged to properly process the details. Therapists are expected to cover fifty-one various subjects, as well as yet most sessions just take around a hr. Reverse mortgages are extremely pricey and must just be made use of as a financing of last resort. The continuous costs are usually funded right into the car loan as well as seniors might be uninformed of just exactly how quickly the fees accumulate. In a lot of cases, choices such as Home Equity Lines of Credit, or other state and also local programs may offer seniors a far better option. Commonly, when the last continuing to be consumer living in a reverse mortgage building dies, the FHA calls for loan servicers to send a letter revealing the balance of the funding due.